Blades of light piercing the dark COVID-19 clouds at last! The Pfizer, Moderna, and Astra-Zeneca vaccines are inching closer to altering for the better our post-COVID-19 near future. There are still formidable problems of access, financing, and logistics but we could soon be departing the territory of crippling catatonia. Our challenge is to craft a recovery that equips the economy towards long-term growth that leads to a speedier Organisation for Economic Co-operation and Development (OECD) membership.

I cannot, for example, wrap my brain around the timing of the Department of Finance-crafted and Senate-approved CREATE (Corporate Recovery and Tax Incentives for Enterprises) bill to give away P625 billion over five years (P42 billion this year alone) in tax revenues to large corporations while the government is scrimping on its anti-COVID-19 spending program and frantically scrounging to borrow P73.2 billion for vaccine purchase and administration!

Also a mystery to me is why the Bangko Sentral ng Pilipinas (BSP) is reducing the policy rate by 0.25% thus putting the real interest rate at -0.5% and risking another asset bubble, knowing that banks and corporations, rather than lending to the private sector, are flocking to riskless government assets. The three-month T-bill rate has dipped to 0.96%, still viewed as a better option than lending to SMSEs. I have always maintained the Keynes doctrine that in an economic crisis, money in the hands of the government is closer to effective demand and employment creation than money in the hands of the private sector whose bottom-line motive is best served with pro-cyclical behavior.

Finally, it is a puzzle to me that while we are trying to attract a bigger share of the re-balanced global FDI, we are stabbing Philippine Economic Zone Authority (PEZA) locators and exporters in the back with two daggers: a higher effective income tax rate via CREATE and an irresponsible peso appreciation. Incoherence, thy footprint is everywhere!

Vietnam by contrast is a template for coherence: not just in its anti-COVID-19 program but more especially in its chosen pathway for long-term post-COVID-19 growth. It is a safe bet that Vietnam will soon put the Philippines in its rear-view mirror if it hasn’t already, and beyond that attain the holy grail of development: convergence with the OECD community in three to four decades.

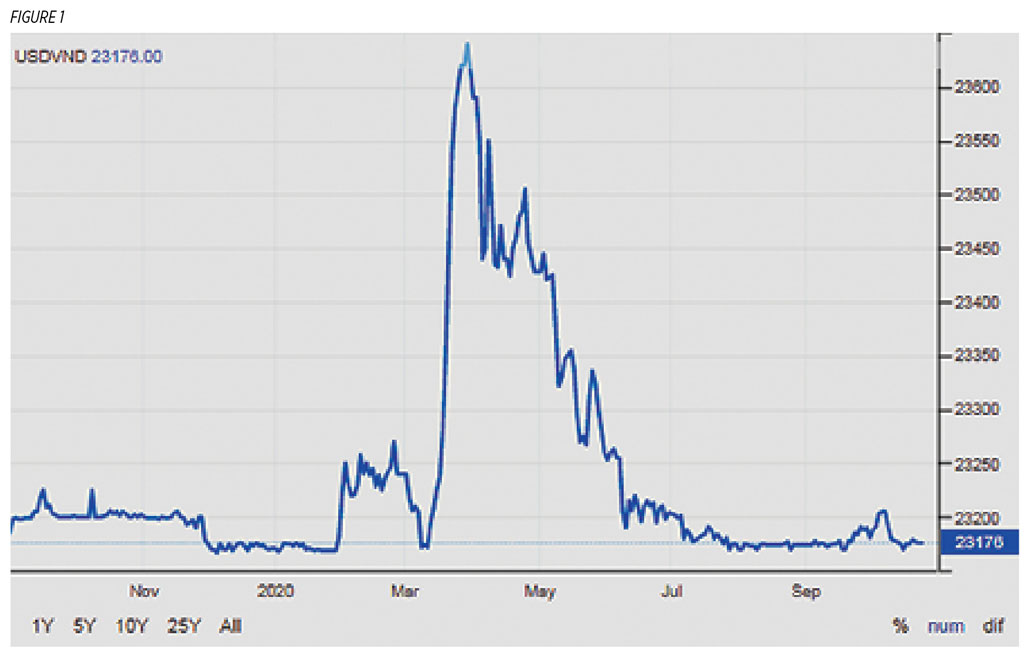

Vietnam has positioned itself as the premier direct foreign investment (DFI) destination in the world and they have come flocking. Why? Because coherence is the middle name of Vietnam’s investment ecology. What does the Vietnam package of policies contain? It has clearly and correctly decided to treat Tradables differently from Non-Tradables: Vietnam distinguishes between its new foreign investment (mostly Tradables and Manufacturing) and old investment (mostly Non-tradables). For the former, a 17% CIT for 10 years with a waver (0%) in the first two years and 8% for the next four reverting to 17% in the ultimate four years; a 20% CIT applies for the latter. While that is bold, it will be futile if export-oriented foreign investors know that they can lose the benefits through future currency appreciations. The Vietnamese authorities have signaled their commitment to reject the all-too-familiar and sneaky practice of “giving with one hand and taking away with the other” by resolutely refusing to let the Vietnamese Dong appreciate as shown by the 2020 trajectory of the Dong/US$. (See Figure 1.)

This is fortitude made manifest — in the face of Vietnam’s growing trade surplus and GIR and in defiance of the US Treasury Department probe to declare it a “currency manipulator” for allegedly undervaluing the Dong at 5% against the US dollar already in 2019 (Lawder D., 25 August 2020, https://fr.reuters.com/article/idUKL1N2FR159). Vietnam has effectively demonstrated to the world a credible commitment to live by its word to its foreign investors. Being able to give costly credible commitments to contract partners is the most important signal of stable governance. Global investors responded and how. This year to September, Vietnam received $14 billion DFI which is only 3% lower than that of 2019’s to September! UNCTAD reports a 24% drop in DFI for the Philippines and no better in the rest of the ASEAN region. The trajectory of the Philippines’ own peso-dollar exchange rate in the year of the pandemic 2020 stands in sharp contrast to that of Vietnam’s (see Figure 2).

The lack of backbone suggested by the Philippine peso/dollar trajectory in Figure 2 is actually the herd response in the region. Vietnam’s fortitudinous coherence stands out like a beckon and reaps its just rewards.

Since CREATE is almost a done deal, we should in future legislation work to correct its incoherent features: as long as we need foreign investors, we should make the corporate income tax (CIT) reduction for PEZA exporters 17% rather than 25% which applies to the rest. The CIT equivalence of the 5% gross income tax (GIT) is 17% CIT as per the Department of Finance (DoF) estimate, which is also the Vietnam rate for new entrants; we should partly remedy the supply push frailty of CREATE by making large corporations “earn” the CIT reduction bonanza by some investment pre-condition such as solar PV installation mounted on idle rooftops; we should counterbalance the inherent unfairness of CREATE by including a debt condonation provision for farmer beneficiaries of the Comprehensive Agrarian Reform Program. The bar against an exchange rate policy that coheres with our high investment ambition and with our keeping the faith with our export investors exists only in the minds of our central bankers. Needless to add, the Philippine economy could use a bigger anti-COVID-19 budget sought by Bayanihan III.

Raul V. Fabella is a retired professor of the UP School of Economics, a member of the National Academy of Science and Technology, and an honorary professor of the Asian Institute of Management. He gets his dopamine fix from bicycling and tending flowers with wife, Teena.